Article

Digital Experience for Financial Services in Mexico

Banks, insurers and fintechs in Mexico build digital experience with Adobe Experience Cloud: unified data, orchestrated journeys and security.

On this page

- Experience Is the New Financial Product

- What Makes Digital Experience in Financial Services Different?

- The Challenges Specific to Mexico's Financial Sector

- How It Is Solved with Adobe Experience Cloud

- 1. A Single Customer View with Adobe Experience Platform

- 2. Audience Activation with Real-Time CDP

- 3. Journey Orchestration with Adobe Journey Optimizer

- 4. Personalization That Respects Privacy

- 5. The Security and Compliance Layer

- Fragmented vs. Orchestrated Financial Experience

- Commerce Is Also Part of the Financial Experience

- The Risks of Getting It Wrong (and How to Avoid Them)

- How We See It at WolfSellers

- Related Services

Experience Is the New Financial Product

For decades, a financial institution competed on rate, coverage and branch network. That terrain still matters, but it is no longer where the customer is won or lost. Today a Mexican consumer chooses — and abandons — a bank, an insurer or a fintech based on how it feels to operate with them: how fast they open an account, whether the app recognizes them, whether the offer they receive makes sense or ignores them.

Mexico's financial sector is going through an accelerated transition. Traditional banking is digitizing processes that were in-person for years; insurers are fighting for relevance in a low-penetration market; and fintechs are entering with 100% digital experiences that reset everyone's expectations. At the center of that fight there is just one thing: the customer experience.

At WolfSellers we work with these institutions from what matters: how to build digital experiences that earn trust, comply with regulation and personalize without compromising privacy — all on Adobe Experience Cloud. This note is our read of the sector and how it is solved with technology.

What Makes Digital Experience in Financial Services Different?

Digital experience in financial services is the set of interactions — onboarding, inquiries, transactions, service, offers — a customer has with an institution through digital channels. It sounds the same as in retail, but there is a fundamental difference: here the customer hands over their money and their most sensitive data, and does so under a strict regulatory framework.

That imposes constraints that do not exist in other sectors:

- Trust is the product. No one leaves their wealth in the hands of an app that feels fragile or unclear.

- The data is sensitive and regulated. Financial and personal information subject to CNBV oversight and personal-data protection rules.

- Omnichannel is mandatory, not optional. The customer starts in the app, calls the call center and ends up at a branch — and expects all of them to know who they are.

- The competition no longer has branches. Fintechs compete on pure experience, without the friction of legacy technology.

That is why the right question is not "how do I make a prettier app?" but "how do I build a digital relationship the customer feels is secure, coherent and relevant?".

The Challenges Specific to Mexico's Financial Sector

Before talking about technology, it is worth naming honestly the challenges we see again and again in banking, insurance and fintech in Mexico:

| Challenge | Why it is hard in finance |

|---|---|

| Trust and security | A single breach or fraud erases years of reputation |

| Regulatory compliance (CNBV) | The experience must be agile without skipping controls or traceability |

| Sensitive data | Personalizing requires using data that, mishandled, is a legal risk |

| 100% digital onboarding | Opening an account without a branch means KYC, identity validation and anti-fraud in seconds |

| Real omnichannel | App, web, call center and branch usually live in silos that do not talk |

| Fintech pressure | Digital-native players redefine what the customer considers "normal" |

| Personalization with privacy | Offering what is relevant without crossing into the invasive or unconsented |

The pattern is clear: the financial sector needs fintech-grade speed and personalization, with the control and governance of a regulated institution. Those two goals are usually seen as opposites. They are not — but reconciling them requires a data and experience architecture built for it.

How It Is Solved with Adobe Experience Cloud

This is where the conversation moves from problem to solution. The reason we recommend Adobe Experience Cloud to the financial sector is not the brand: it is that it solves, in a single governed platform, the three fronts that cost the most — unified data, journey orchestration and secure personalization.

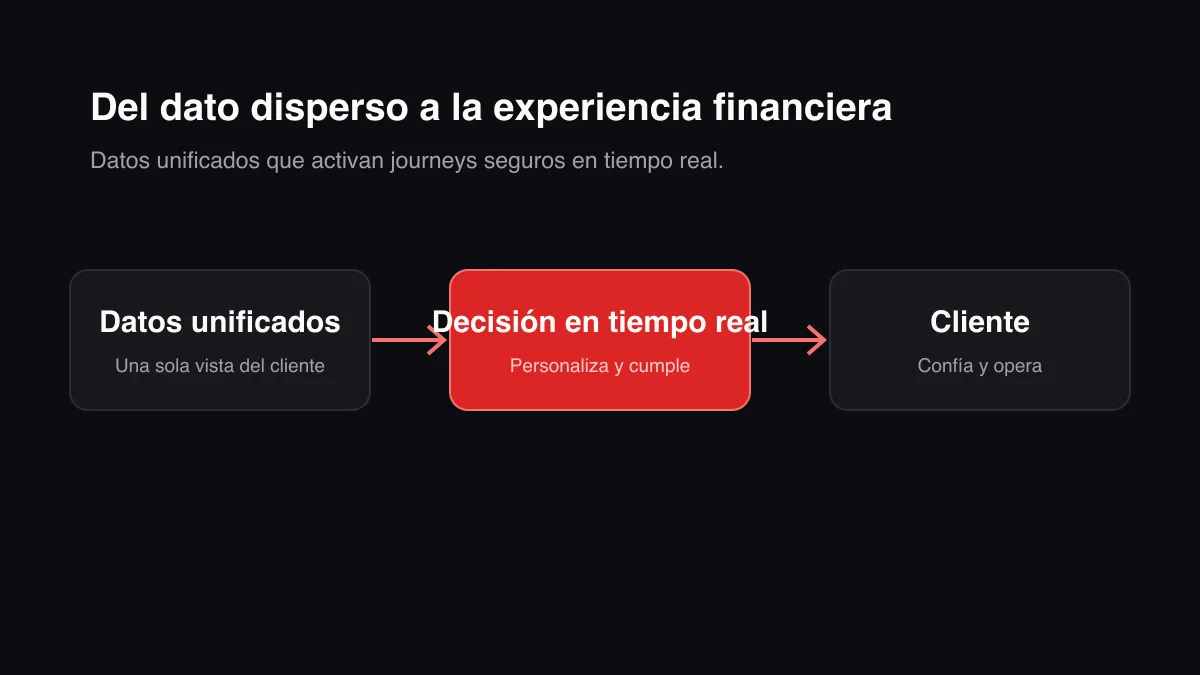

1. A Single Customer View with Adobe Experience Platform

The root problem in almost every financial institution is the same: the customer's data is fragmented. The core banking system knows their balances, the CRM knows their complaints, the app knows their behavior, and none of them talk to each other. The result is a customer who feels like a stranger to their own bank.

Adobe Experience Platform solves this by building a real-time unified profile: it integrates signals from every channel and system into a single coherent view of the customer, governed and with control over which data can be used and for what. It is the foundation — without it, everything else is makeup.

2. Audience Activation with Real-Time CDP

Having unified data is useless if you cannot act on it. Adobe Real-Time CDP takes that profile and lets you build precise audiences and activate them in real time across the right channels — with built-in data governance, which in finance is non-negotiable.

This is what allows you, for example, to stop sending the same credit promotion to everyone and start reaching the right customer, with the right offer, respecting their consents and without exposing sensitive information.

3. Journey Orchestration with Adobe Journey Optimizer

Financial relationships are not an event, they are a continuous journey: onboarding, activation, cross-sell, retention, collections. Adobe Journey Optimizer lets you design and orchestrate those journeys end to end, reacting to what the customer does in the moment they do it.

A few cases where we see it generate direct value in the sector:

- Digital onboarding. Guiding the new customer step by step until they activate and use their product — the most fragile moment of the entire relationship.

- Smart collections. Reminders and payment journeys with the right tone and channel, instead of a generic call that erodes the relationship.

- Contextual cross-sell. Offering the right insurance or credit product when the customer's behavior signals it makes sense — not through a mass campaign.

4. Personalization That Respects Privacy

Personalization in finance walks a fine line: relevance builds trust, intrusion destroys it. The advantage of doing it on Adobe is that personalization relies on the governed profile in Experience Platform, where consent and data-use rules travel with the data. You personalize with what the customer allowed, not with everything you have.

5. The Security and Compliance Layer

None of the above is viable in finance without a solid foundation of security and compliance. Operating experiences on sensitive data requires robust authentication, access control, traceability and a posture aligned with CNBV regulation and data-protection best practices. At WolfSellers we treat it as an inseparable part of the design — not a patch at the end — leaning on our cybersecurity practice. Digital openness without governance is a risk; governed openness is a competitive advantage.

Fragmented vs. Orchestrated Financial Experience

The difference between an institution that suffers these challenges and one that turns them into an advantage is best seen side by side:

| Fragmented experience | Orchestrated experience |

|---|---|

| Each channel has its own version of the customer | A single unified profile, consistent everywhere |

| Mass campaigns identical for everyone | Precise audiences activated in real time |

| Onboarding with friction and abandonment | A guided journey that takes the customer to activation |

| Generic collections that damage the relationship | Contextual collections, in the right channel and tone |

| Blind (or no) personalization | Personalization with consent and data governance |

| Security as a patch at the end | Security and compliance by design |

| The fintech sets the pace | The institution competes with its own experience |

The takeaway is direct: technology does not replace trust or regulation — it makes them operable at scale. That is what lets a bank or an insurer compete with the agility of a fintech without giving up its governance.

Commerce Is Also Part of the Financial Experience

A front that is often underestimated: financial institutions increasingly sell and operate products like a digital commerce business. Buying insurance, opening a line of credit or acquiring an investment product looks more and more like an e-commerce checkout — and should feel just as fluid.

This is where Adobe Commerce (formerly Magento) enters the financial conversation: an API-first platform to build those contracting and digital-sales flows with the same transactional solidity. And looking ahead, it is worth understanding how AI agents will start to operate these decisions too, something we cover in our note on agentic commerce.

The Risks of Getting It Wrong (and How to Avoid Them)

Let's be honest — in finance, a poorly built digital experience does not just disappoint, it exposes:

- Personalizing on ungoverned data. Using customer information without consent control is a regulatory risk before it is an experience problem. Order matters: data governance first, personalization second.

- Digitizing friction instead of removing it. Moving a bureaucratic process into an app does not fix it — it just makes it bureaucratic and digital. The goal is to redesign the journey, not trace it.

- Treating security as a final phase. In a sector where a breach erases years of reputation, security and compliance are designed from day one, not added at the end.

The failure pattern is always the same: treating digital experience as a cosmetic layer, when in finance it is a change in data architecture, operations and governance.

How We See It at WolfSellers

Our conviction is simple: in financial services, the experience the customer perceives is as important as the product they contract — and both are built on the same foundations: unified data, orchestrated journeys and security by design.

The urgency is real. According to data from Adobe together with Oxford Economics, 78% of organizations expect agentic AI to manage most of their interactions within the next 18 months, yet only 16% have it implemented, only 51% have adequate cloud infrastructure and 75% name data quality as their main limitation. The takeaway for a financial institution is direct: the intent exists, but most still lack the data and the architecture to operate the experience the market already expects.

That is why we work with banks, insurers and fintechs not only as technology implementers, but as a strategic partner: we help define what experience you want to build and what you are missing to achieve it, and then we build it with Adobe Experience Cloud. If you want to go deeper into how digital experience is becoming orchestrated end to end, we cover it in our note on Digital Experience 2026.

The financial experience of the future does not ask whether your app is pretty. It asks whether your institution knows, protects and accompanies every customer coherently. That is the conversation worth having now. Let's talk.

Related Services

If this topic is relevant to your institution, these WolfSellers services can help you implement it: